I’ve only been taking a serious run at retirement for the past two years, but one thing has become crystal clear:

Maintaining good credit is just as important after retirement as it is while you’re working.

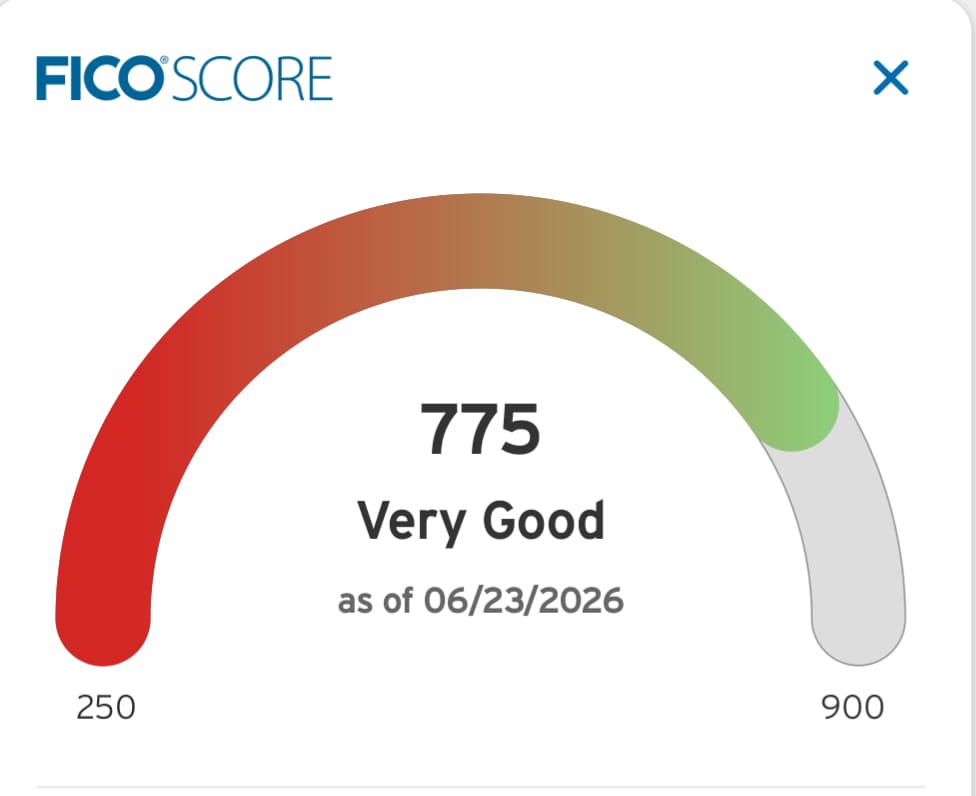

My credit score has consistently stayed between 750 and 775 for as long as I can remember, and I’m glad I made it a priority.

Even though I’m no longer relying on a regular paycheck and playing myself now, good credit still makes my life easier—whether it’s qualifying for health insurance, getting the best interest rates, renting a car, or simply having financial flexibility when I need it.

Retirement doesn’t mean your financial reputation retires too. In many ways, it becomes even more valuable.

One financial tool I’ve occasionally taken advantage of is a credit card balance transfer when I needed a little extra flexibility.

Ideally, I wouldn’t have to rely on a balance transfer at all,

My “very good” credit score just gives me options depending on my current financial situation vs the market.

I’m still learning what consistent retirement spending really looks like, and there have been times I’ve leaned on this option more than I probably should have.

Every once in a while, one of my credit card companies sends me a balance transfer offer that’s simply too good to ignore—often with a very low promotional interest rate for a set period.

It’s important to understand that a balance transfer is not the same as a cash advance.

Cash advances usually come with high interest rates that begin accruing immediately, along with additional fees.

A promotional balance transfer, on the other hand, can provide temporary breathing room if it’s used responsibly and you have a plan to pay it off before the promotional rate expires.

Like any financial tool, it can be helpful—or harmful if not used properly.

The key is understanding the difference and using it as part of a plan, not as a long-term solution.

Here’s a real example.

I received a balance transfer offer for $3,000 USD with a 5% processing fee.

I like to keep the amount under the offer, so for example purposes I asked for $2850.

That means the fee is $142.50, so the total balance is under $3000.

In other words, I’m paying $142.50 for up to twelve months of financial flexibility .

Broken down over a year, that’s only about $12.50 per month while my retirement accounts have been yielding well over 5%.

As long as I pay the balance off before the promotional period expires, that’s the only cost I’ll pay.

For me, that’s a reasonable price for some short-term breathing room while I continue refining my retirement budget.

I fully realize I’m flushing $142.50 down the toilet when I could be using my own money.

But, I also realize that, in the grand scheme of things, it’s flyspeck compared to what my investment portfolio is earning right now.

Of course, markets can change at any time, and I’m well aware of that scenario too.

The difference is that I have an plan that will cover it.

I would have twelve months to pay off this balance transfer, and it only costs me about $12 a month in fees while monitoring my investments.

That’s a small price to pay for the flexibility it gives me while I continue fine-tuning my retirement budget.

Is it ideal? No.

Is it part of my long-term strategy? Let’s see how the math works out!

But as a short-term financial tool to tap the breaks on my spending and catch up.

I’m comfortable using as I continue learning what retirement really costs.

Many promotional balance transfers, interest isn’t necessarily retroactively charged, but once the promo ends, the remaining balance is subject to the regular APR.

The difference would be tragic if you were left with ~$700 in interest plus whatever remaining amount is left on the loan.

That is why retail store often do to their Customers!

Eventually a $3000 couch, TV etc is $3800, OUCH!!

As with any financial tool, the key is understanding the fine print and having an exit plan before you ever sign up.